Cybersecurity in 2025: Why Protecting Your Business Is No Longer ‘Optional’

In an age where digital tools drive almost every part of business, cyber threats are rising faster than ever and

In an age where digital tools drive almost every part of business, cyber threats are rising faster than ever and

From Left: Hayden Cush, General Manager – AFG Home Loans & Matthew Ikin, Executive General Manager – We Money AFG

Take your business from good to great by implementing processes that save time, save money and deliver better customer experiences.

Australian Finance Group Ltd’s (AFG) non-bank lending business, AFG Securities, has today announced the launch of AFG Home Loans Retro Thrive, an interest-only refinancing mortgage

Tired houses are a yawn for their occupants and potential buyers when the time comes to sell. We look at some of the simpler ways

Saving can be simple when you know how. Yes, sacrifice is needed to get ahead but you can also be frugal without being a total

When it comes to buying a house, the kitchen is one of the most important features home buyers take into consideration. If your kitchen is

Is the Great Australian Dream to own your own home over? That’s the question on the lips of Millennials around Australia… and indeed many of

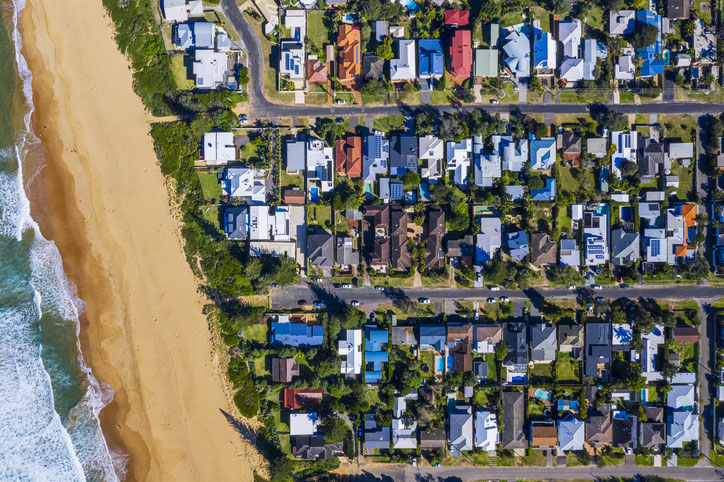

If Dorothea Mackellar was here today she might replace her famous poetry line about “ragged mountain ranges” with one about the country’s home price ranges.

Christmas is a magical time of year but it’s all too easy to get caught up in the holiday hysteria and end up spending much

While prices are a product of supply and demand, it’s worth understanding the factors that sit beneath both sides of the equation. In other words,

While you’re getting your head around the macro, don’t lose sight of the micro. Median house prices can vary greatly from suburb to suburb. Here’s

It’s no secret tax deductions, in addition to capital gains, remain a carrot for property investors. But tax rules have tightened, and the landscape is

In an age where digital tools drive almost every part of business, cyber threats are rising faster than ever and